After reading A Beginner’s Guide to Investing by Alex Frey, I liked the idea of having a small investing “sandbox”. Rather than micro-managing the bulk of your investments on a day-to-day basis, the author recommends having a small sandbox for some portion of your investments which you’re allowed to day-trade and actively manage.

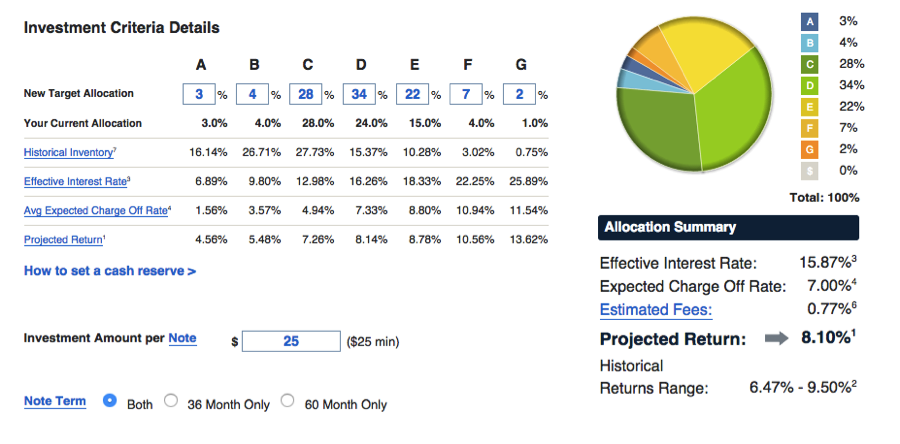

I had heard about Lending Club for a while, and it piqued my interest. For those not familiar, Lending Club allows investors to invest in smaller fractions of loans to borrowers (called “notes”). On a monthly basis, the investor receives back principal and interest on the notes they have invested in, assuming the borrowers pay on time and don’t default. The Lending Club website advertises that investors receive an average annual ROI of 8.10% for D-G weighted portfolios (see figure below) and that 99.9% of investors that diversify among at least 100 notes see positive returns. As a scientist, I appreciated the amount of data they had on their website, and spent a lot of time looking through their interactive investor performance graph and even the downloadable spreadsheet data they publish on a quarterly basis.

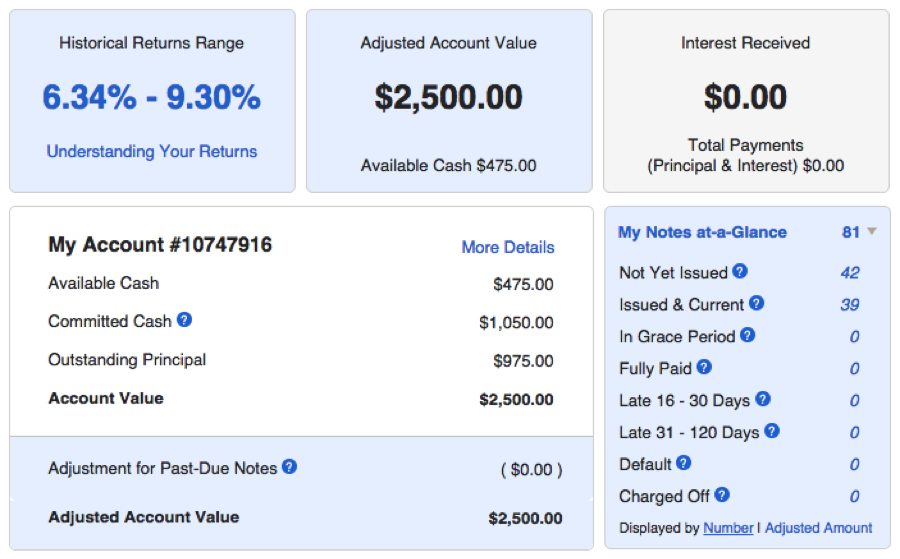

I decided to put $2,500 aside into Lending Club so I could invest in 100 $25 notes. After 5 days waiting for my money to get deposited in my new Lending Club account, I chose to set up Automated Investing using the following Investment Criteria (called “D-G Weighted”):

**Note: Every Lending Club loan is assigned an investment “grade” which determines the perceived risk of the loan (G being the highest risk) and the interest rate. Higher risk loans also have the investment reward of higher returns, which is offset by the expectation that the charge-off rates (the rate at which borrowers “default”) on the loan will be higher.

In addition to the Investment Criteria above, I also set up an additional filter for my Automated Investing, based on some data analysis I had done of Lending Club’s 2007-2011 data:

- Loans must not have any public records.

- I chose to invest in loan purposes that appeared to have the lowest charge-off (default) rates: Refinancing credit cards, consolidate debt, home improvement project, wedding expenses, paying for dream vacation, covering moving expense, home down payment, car financing, and major purchases.

Lending Club warns that Automated Investing might not order notes very quickly if you have stringent filters, due to limited inventory. To speed up the initial investing process along, I had to manually ordered several notes. But even then, by the end of Day 1, I only was able to invest $1525 of my $2500. I was a little disappointed at how long it was taking to getting my investments in place.